Monefit SmartSaver Review 2026: €5 Welcome Bonus + 0.5% Cashback on Up to 10.52% APY

Most P2P lending platforms require you to pick individual loans, configure auto-invest rules, and actively manage your portfolio. Monefit SmartSaver takes a different approach entirely. You deposit money, and it starts earning. That is it.

We have been using Monefit SmartSaver for several months now, and what stands out most is how remarkably simple the whole experience is. The interface is clean, deposits take seconds, and returns show up daily in your account. For European investors looking for a hands-off way to earn attractive interest on their savings, this is one of the most compelling options available right now.

Monefit also runs a sign-up incentive worth knowing about: a €5 welcome bonus credited after registration, plus 0.5% cashback on every deposit (0.25% credited instantly, 0.25% credited after 90 days). It stacks on top of the regular interest rate. We cover the full breakdown further down.

In this review, we cover everything you need to know: how it works, what it pays, the risks involved, and whether it deserves a spot in your portfolio.

What Is Monefit SmartSaver?

Monefit SmartSaver is an investment product operated by Monefit Investments OÜ, an Estonian company that is 100% owned by Creditstar Group AS. Creditstar has been in the consumer lending business since 2006, operating across 8 European countries with over 1.4 million registered clients. Their financials are audited by KPMG, which adds a layer of credibility that many P2P platforms lack.

The way it works is straightforward. When you deposit money into SmartSaver, your funds are used to finance consumer loans issued by Creditstar Group entities across Europe. Technically, you are purchasing "SmartSaver Claims" via assignment agreements, meaning you acquire claims from consumer credit agreements. Monefit then services those claims on your behalf.

The key difference from traditional P2P platforms like Mintos is that you never have to choose which loans to invest in. There is no marketplace, no filters, no manual selection. You deposit your money, and the platform handles everything automatically.

Since launching in October 2022, the platform has grown to over 30,000 investors, with more than EUR 302 million invested in total and over EUR 18 million in returns paid out. They maintain a 100% payout success rate since launch, which is a strong track record for a platform of this age.

Interest Rates: Flexible and Vault Options

Monefit SmartSaver offers two ways to earn returns, and this flexibility is one of its strongest features.

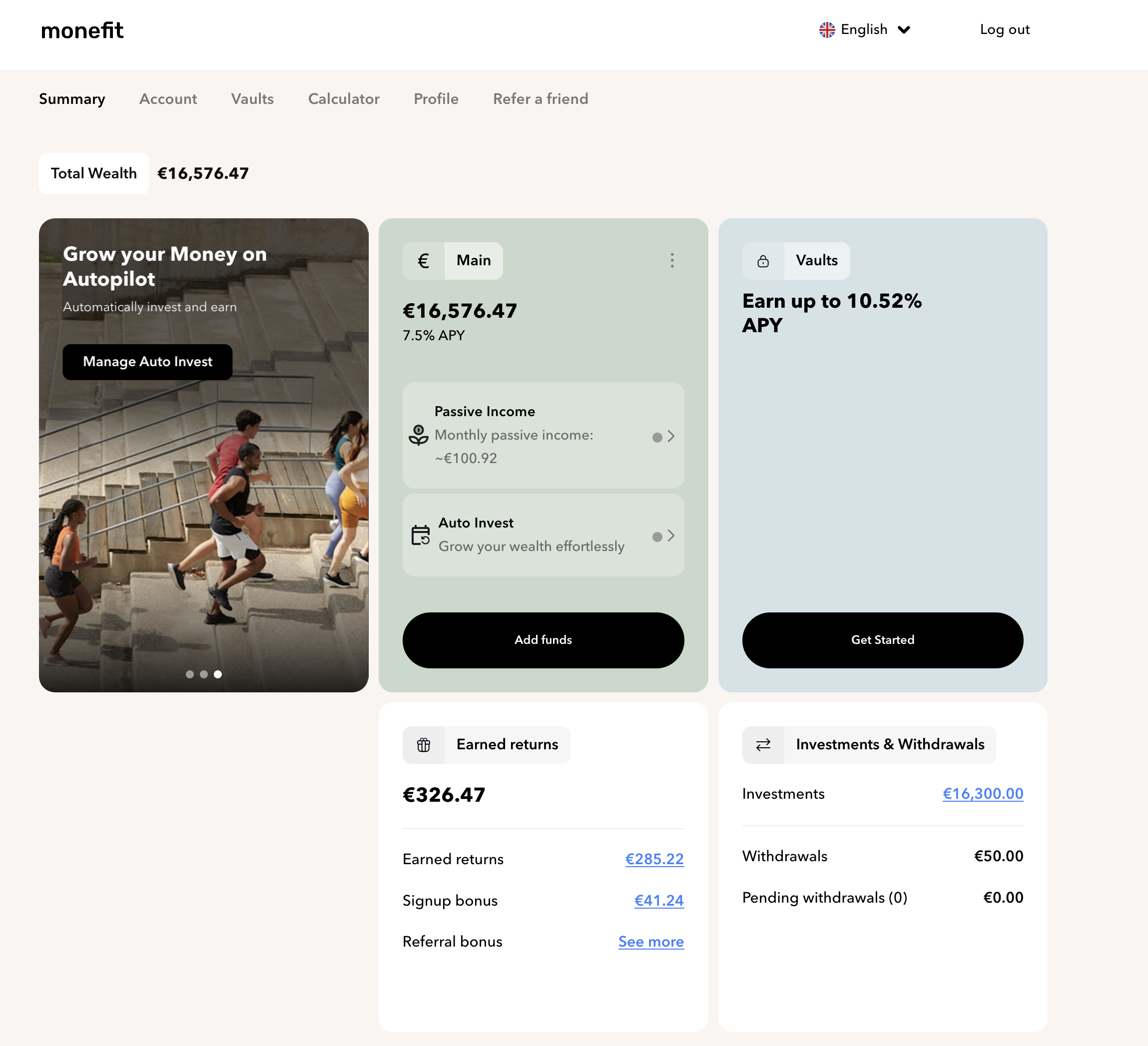

Main Account (Flexible Terms)

The Main Account currently pays 7.50% APY with no lock-up period. Returns are calculated and paid daily, and you can withdraw your funds at any time (subject to the withdrawal limits we cover below). The rate was actually increased from 7.25% to 7.50% in June 2025, which goes against the broader trend of declining rates across the industry.

For context, this is significantly higher than what most high-yield savings accounts in Europe offer (typically 2-3%) and also beats Bondora Go & Grow, which currently pays 6.00% APY after cutting from 6.75% in April 2025.

We personally use the flexible terms for most of our balance because the combination of 7.50% interest and the ability to withdraw at any time is very attractive. It strikes the right balance between return and accessibility.

Vaults (Fixed Terms)

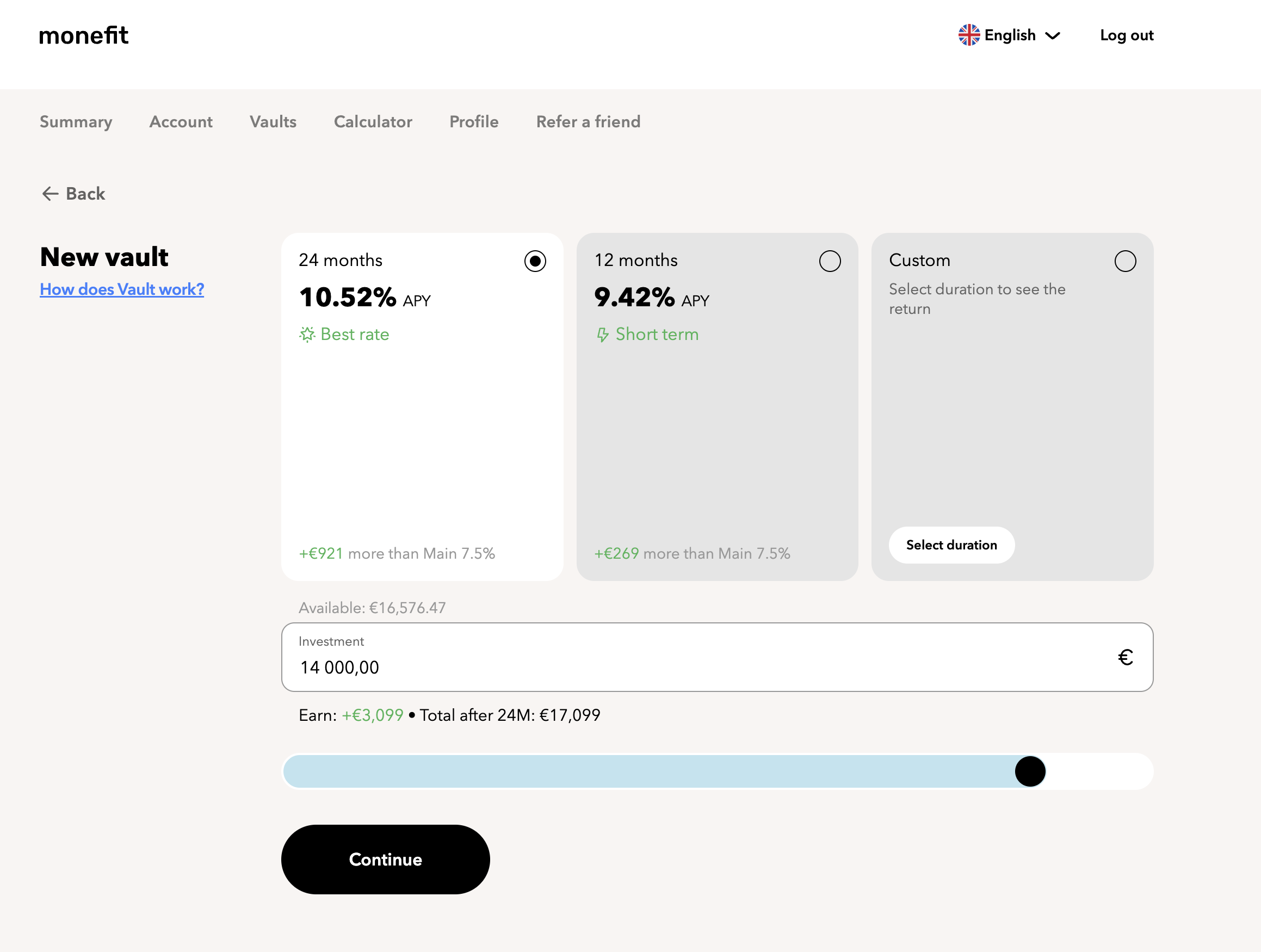

If you are willing to lock up your funds for a set period, the Vaults offer even higher returns:

- 12 months: 9.42% APY

- 18 months: 9.96% APY

- 24 months: 10.52% APY

As of May 2026, Vaults shorter than 12 months are no longer available for new investments.

The Vault system is well-designed. You can choose an exact maturity date via a calendar, and after opening a Vault, you have a 10-day window to add more funds before it locks. There are three auto-renewal options: reinvest the full balance, reinvest capital only, or no renewal at all.

All Vaults and the Main Account now offer an optional monthly payout, so you can lock money into a higher-return Vault and still receive cash flow without waiting until maturity. Earnings across the Main Account and any eligible Vaults are combined into a single payment sent to your bank account on the 1st of each month.

The Vault creation screen lays out the available terms side by side: 24 months at 10.52% APY flagged as the Best rate, 12 months at 9.42% APY, and a Custom duration picker for anything in between. You can also see how much extra you would earn versus leaving the same balance in the 7.5% Main Account, which makes the trade-off between flexibility and yield easy to weigh up.

One important caveat: if you close a Vault early, you lose all accumulated returns. There is no partial penalty. You forfeit everything earned, and there is a 30-day cooldown before funds return to your Main Account. This is quite harsh compared to simply accepting a lower rate for early withdrawal, so only lock up money you are genuinely comfortable not touching.

Our Experience: Dashboard and Ease of Use

The first thing you notice when logging into Monefit SmartSaver is how clean everything is. The dashboard gives you an immediate overview of your total wealth, current Main Account balance, earned returns, and any bonuses received.

In our account, we can see the total wealth at a glance, with the Main Account earning 7.5% APY. The dashboard also shows earned returns and any signup bonus separately, which is a nice touch for tracking exactly where your money is coming from. The €5 welcome bonus and the 0.5% cashback on deposits are credited automatically, so you can watch them land in real time.

Adding funds is equally straightforward. You choose your amount, pick between card payment (instant) or bank transfer (1-3 business days), and confirm. There is also an Auto Invest feature that lets you set up recurring deposits on a daily, weekly, or monthly basis directly from a saved card, which is great for building a savings habit without thinking about it.

One thing to note: SEPA bank transfers are free, but card deposits now carry a 1% fee (introduced January 2026). However, the Auto Invest feature is exempt from this fee, so if you set up recurring card deposits through Auto Invest, you avoid the charge entirely. During your first 7 days after verification, all card deposits are also free.

Withdrawal Terms

This is where Monefit SmartSaver has some limitations worth understanding.

You can withdraw up to EUR 1,000 per calendar month instantly. This was introduced in November 2025 and was a significant improvement over the previous system where all withdrawals had processing delays.

For amounts above EUR 1,000, withdrawals take up to 10 business days to process, plus 1-3 additional business days for the bank transfer to reach your account. There are no withdrawal fees from Monefit's side, and interest continues accruing during the withdrawal processing period.

The minimum withdrawal is EUR 50 (or your full balance if it is under EUR 50), and the maximum per transaction is EUR 50,000.

For comparison, Bondora Go & Grow allows unlimited daily withdrawals with no cap, which is a clear advantage on the liquidity front. If instant access to larger amounts is a priority for you, that is worth considering. We have a dedicated comparison below.

Monefit SmartSaver vs. Bondora Go & Grow

These two platforms are the most direct competitors in the European "deposit and earn" savings space. Both offer a simple, automated experience without manual loan selection. Here is how they compare on the metrics that matter.

The bottom line: Monefit wins on yield (7.50% vs. 6.00%, a 1.5 percentage point gap that widened after Bondora's April 2025 rate cut) and offers fixed-term Vaults that Bondora simply does not have. Bondora wins on liquidity with unlimited instant withdrawals and has a longer track record. If you prioritize returns and are comfortable with the EUR 1,000/month instant cap, Monefit is the stronger choice. If instant access to your full balance is non-negotiable, Bondora remains the safer bet on that front.

Is Monefit SmartSaver Safe?

This is the most important question, and it deserves an honest answer.

Monefit SmartSaver is not a bank account. It is not covered by any EU deposit guarantee scheme, meaning your funds are not protected up to EUR 100,000 the way a traditional savings account would be. The platform states clearly that "no guarantees are offered for investments made with SmartSaver."

That said, there are several factors that work in its favor:

Creditstar Group's track record. The parent company has been operating since 2006, making it one of the more established players in European consumer lending. Their lending subsidiaries are regulated in each country they operate in, including by the Estonian Financial Supervisory Authority, Finland's FIN-FSA, Sweden's Finansinspektionen, and the Czech National Bank, among others.

Loan collateralization. Approximately 64% of Creditstar's loan portfolio (around EUR 150.7 million out of EUR 235 million) is collateralized. This means that even in a default scenario, there are underlying assets that could be recovered.

Financial health. Creditstar Group reported total assets of EUR 367 million in 2024, with a net loan book of EUR 351.2 million (up 27% year-on-year). Their equity-to-assets ratio improved from 19.22% to 21.68%. Net profit was EUR 7.3 million, down from EUR 10 million in 2023, though this was attributed to the transition to IFRS reporting standards rather than operational issues.

ECSP license. Monefit obtained an EU crowdfunding service provider license in February 2024, which provides a regulatory framework. While this is not equivalent to full banking supervision, it is a meaningful step above being entirely unregulated.

Concentration risk. All invested funds flow to a single loan originator (Creditstar Group). This is different from platforms like Mintos where you can diversify across multiple originators. If Creditstar were to face financial difficulties, all SmartSaver investments would be affected.

The average loan issued by Creditstar carries a 26% interest rate with a 15-month term. The spread between that 26% and what they pay investors (7.5-10.52%) covers their loan loss reserves, operating costs, and profit margin. This healthy spread is one reason the platform has been able to maintain its payout record.

Pros and Cons

How to Get Started with Monefit SmartSaver

The sign-up process takes less than 10 minutes. Here is a step-by-step walkthrough.

€5 Welcome Bonus + 0.5% Cashback

If you sign up through our link, you receive a €5 welcome bonus credited after registration, plus 0.5% cashback on every deposit you make. The cashback is split: 0.25% credited instantly when you deposit, and another 0.25% credited after 90 days.

To give you a sense of scale: if you deposit EUR 10,000, you would earn EUR 50 in cashback (EUR 25 instantly, EUR 25 after 90 days) on top of the interest you are already earning, plus the €5 welcome bonus.

The promotion stacks with the regular interest rate, meaning you earn 7.50% APY on your Main Account on top of the cashback and welcome bonus. There is no promo code needed. Simply use this link to sign up and the incentives are applied automatically.

Who Should (and Shouldn't) Use Monefit SmartSaver

Monefit SmartSaver is a good fit if you:

- Want to earn significantly more than bank savings rates without active management

- Are comfortable with the risks of P2P-style lending products

- Do not need instant access to more than EUR 1,000 per month

- Are a European resident (available in 31 EEA countries plus Switzerland)

- Want a clean, simple platform without the complexity of traditional P2P marketplaces

It may not be the right fit if you:

- Need instant access to large amounts at any time (consider Bondora Go & Grow instead)

- Want deposit guarantee protection on your savings

- Prefer to diversify across multiple loan originators

- Need a mobile app for managing your investments on the go

Here is a video about Monefit SmartSaver for a more detailed look:

Supported Countries

Monefit SmartSaver is available to residents and citizens of all 31 EEA countries plus Switzerland. This includes: Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, and Switzerland.

The platform supports English, German, Spanish, French, and Estonian languages.

Frequently Asked Questions

Is my money protected by deposit insurance if Monefit or Creditstar goes bankrupt?

No. Monefit SmartSaver is not a bank and is not covered by any EU deposit guarantee scheme. Unlike bank savings accounts that protect up to EUR 100,000, your investment in SmartSaver carries the risk of the underlying loan portfolio. That said, the loans are partially collateralized (around 64%), which means recovery of at least some funds would be possible in a worst-case scenario.

How long does it actually take to withdraw my money?

Up to EUR 1,000 per calendar month can be withdrawn instantly. Amounts above that take up to 10 business days to process, plus 1-3 additional business days for the bank transfer. Interest continues accruing during the withdrawal period. There are no withdrawal fees from Monefit's side.

Is Monefit SmartSaver the same as a bank savings account?

No. Despite the "savings" branding, it is an investment product that funds consumer loans via the Creditstar Group. It carries more risk than a traditional bank savings account but offers significantly higher returns (7.50% vs. typical 2-3% at European banks). Think of it as sitting between a savings account and a full P2P lending platform in terms of both risk and reward.

What happens if everyone tries to withdraw at the same time?

Monefit maintains liquidity reserves, but they acknowledge in their terms that large-scale simultaneous withdrawals could result in delays. In such a scenario, withdrawals would be processed gradually to ensure fairness across all investors. This is a standard risk with any P2P-style platform and is worth being aware of.

Do I need to pay taxes on my Monefit earnings?

No tax is withheld at source. You receive the full amount of your earnings and must declare them in your tax residence country according to local tax regulations. Tax reports are available for download from the platform, making it easy to report your earnings accurately.

How does Monefit SmartSaver compare to Bondora Go & Grow?

Monefit offers higher returns (7.50% vs. 6.00%) but has slower withdrawals for amounts above EUR 1,000 and no mobile app. Bondora provides better liquidity with unlimited daily withdrawals and a longer track record (since 2018 vs. 2022). On welcome bonuses, both platforms give new users €5, but Monefit also adds 0.5% cashback on every deposit. The trade-off is essentially higher yield (and a stronger sign-up incentive) versus better access to your money. You can also use our compound growth calculator to model the difference in returns over time.

Can Creditstar's past payment delays on other platforms happen with Monefit too?

Creditstar did experience some payment delays on the Lendermarket platform in 2022. However, Monefit SmartSaver has maintained a 100% payout success rate over its first 3+ years of operation. The platform is Creditstar's flagship consumer-facing product, so there is a strong incentive to maintain its reputation. That said, past performance does not guarantee future results, and investors should monitor the company's financial reporting.

Is there a Monefit SmartSaver welcome bonus in 2026?

Yes. New users who sign up via our link receive a €5 welcome bonus credited after registration, plus 0.5% cashback on every deposit. No promo code is required, the incentives apply automatically when you use the sign-up link.

How does the 0.5% Monefit cashback work?

The 0.5% cashback is split into two parts. You receive 0.25% credited instantly when your deposit settles, and the remaining 0.25% is credited 90 days later. The cashback applies to every deposit, not just your first one, and stacks on top of the regular Main Account interest rate.

When is the Monefit cashback paid out?

The first 0.25% is credited to your Main Account balance instantly the moment your deposit settles. The second 0.25% is credited automatically 90 days after the deposit, on top of the daily interest you have been earning in the meantime. There is no manual claim step required.

If you want to track your Monefit returns alongside your other investments, a portfolio tracker like Snowball Analytics is a great option. We use it to track our various P2P investments, including Monefit SmartSaver, all in one place.

Final Verdict

Monefit SmartSaver has earned our recommendation as one of the best options for European investors looking to earn attractive returns without the complexity of traditional P2P platforms. The 7.50% flexible rate is the highest in its category, the interface is genuinely a pleasure to use, and the Vault system gives you granular control over your risk-return-liquidity balance.

The platform is not without its drawbacks. The EUR 1,000/month instant withdrawal cap, lack of deposit insurance, and single-originator concentration risk are real considerations. But for money you are comfortable setting aside for the medium to long term, the combination of high returns, daily compounding, and effortless setup is hard to beat. If you are also looking for a traditional stock broker alongside your P2P investments, our BrokerMatch tool can help you find the right fit.

We use it ourselves and have been consistently satisfied with the experience. If it sounds like a fit for your portfolio, you can sign up here and get a €5 welcome bonus plus 0.5% cashback on every deposit.

Trading involves significant risk and may not be suitable for all investors. The value of investments can go down as well as up, and you may lose some or all of your initial investment. Past performance is not indicative of future results.