.png)

How Margin Trading Works at Interactive Brokers: A Complete Guide

Most people hear "margin" and picture a day trader blowing up their account. That reputation is half deserved. Used recklessly, margin is one of the fastest ways to lose money in markets. Used deliberately, it is simply a low cost loan secured against the investments you already own, and at Interactive Brokers it happens to be the cheapest such loan available to ordinary retail investors.

This guide explains exactly how margin works at Interactive Brokers: what it costs, how the interest is charged, why your buying power suddenly shows a number far larger than your cash, and the one mechanic that catches people out, automatic liquidation. We use real worked examples in dollars so you can see the upside and the downside side by side. None of this is a recommendation to use margin. It is an explanation of how it works so you can decide for yourself.

What margin actually is

When you open a standard brokerage account, you can only buy what your cash covers. A margin account changes that. It lets you borrow money from the broker, using the securities you already hold as collateral, to buy more. The loan has no fixed end date and no monthly repayment schedule. You pay interest on whatever you have borrowed, for as long as you borrow it, and you repay whenever you choose by either selling something or depositing cash.

The cleanest way to picture it is this: at Interactive Brokers your cash balance and your margin loan are the same number. When the balance is positive, that is your cash. When it goes negative, that negative figure is your loan. If you hold $100,000 in shares and $200 in cash, then buy another $10,000 of shares, your cash balance simply reads minus $9,800. That is your margin loan. There is no separate loan account to manage and nothing to sign each time.

This is also why so many new users get caught out. Holding a margin account does not mean you are borrowing. You only start paying interest the moment your cash balance turns negative. You can keep a margin account for years and never touch the borrowing function. If you want to understand the account types in more depth, our guide on IBKR Lite vs IBKR Pro covers which tier supports margin and how the pricing differs.

Why your buying power looks enormous

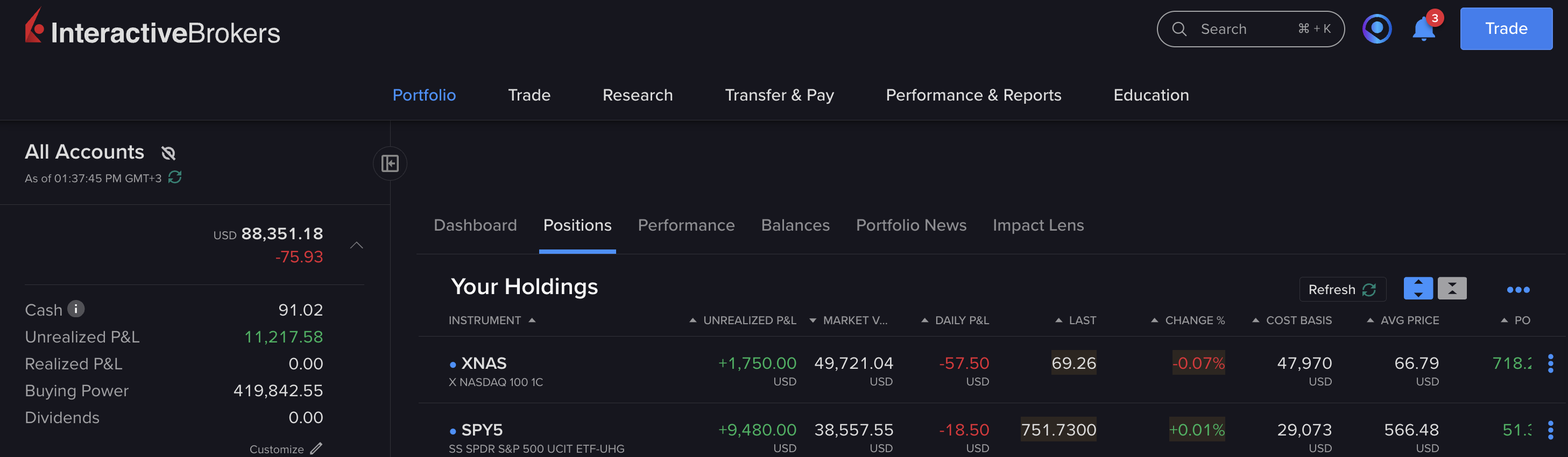

The first thing that startles people after enabling margin is the buying power figure. When we switched our own account over, a balance of around $88,000 suddenly showed more than $400,000 of buying power. That is not a glitch, and it is not money you have. It is the maximum value of securities you could theoretically purchase using maximum margin.

Our own account moments after enabling margin: roughly $88,000 of equity, but more than $419,000 of buying power.

Two things drive that large multiple. First, Interactive Brokers applies a low margin requirement to broad, diversified holdings like major index ETFs, because it views them as lower risk collateral. Second, the figure shown is usually the intraday number, which can be four times your equity or more. For positions you hold overnight, the standard Regulation T rule of 50 percent initial margin reapplies, which means your realistic sustainable ceiling is closer to twice your equity, not four or five times.

The practical takeaway is simple. Ignore the headline buying power number. It is a day trading artifact, and the broker shows it to you because more borrowing earns it more interest. A sensible long term investor borrows a small fraction of what the platform technically permits.

What it costs: Interactive Brokers margin rates

This is where Interactive Brokers genuinely stands apart. Its margin rates are among the lowest available to retail investors anywhere. The rate is built as a benchmark rate (which tracks short term central bank rates and floats with the Fed) plus a fixed spread that shrinks as your loan grows. Here is the current USD schedule for IBKR Pro, verified against the official rates page in May 2026.

For context, many traditional brokers charge somewhere between 8 and 10 percent on comparable balances, so Interactive Brokers can be less than half the cost. The benchmark moves with central bank policy, so when rates fall your margin cost falls automatically within days, and when rates rise it climbs. Note two things from the fine print: there is a minimum floor of 0.75 percent on margin loans, and the rate can carry a small surcharge if financing is not pre arranged, so treat the headline figure as the baseline.

The rate also depends on the currency you borrow. Euro denominated margin is currently cheaper still, with a first tier around 3.4 percent, while sterling sits close to the dollar near 5.15 percent. Because of this, the currency you hold and borrow in matters. Our Interactive Brokers currency conversion guide explains how to avoid accidentally borrowing in the wrong currency, which is a common and costly mistake.

How and when interest is charged

Interest accrues daily on whatever you have borrowed and is posted to your account once a month, on the third business day of the following month. If you keep some cash in the account, the interest is simply deducted from that cash. If you are fully invested with no cash, the interest is added to your loan balance, which then grows slowly over time. There is no penalty, no demand for a payment, and nothing you need to action. The loan just sits in the background like a flexible overdraft secured by your portfolio.

This timing catches people out. When we checked our own statement the day after opening a small margin loan, the only interest line showing was a tiny amount IBKR had actually paid us, interest earned on idle cash earlier in the year, not interest we owed. Our margin interest had not appeared at all yet, precisely because it accrues quietly each day and only lands on the statement the following month. So do not be alarmed if you borrow and see no interest charge immediately. It is coming, it is just on a monthly cycle.

Our cash report the day after the first loan. The only interest line shows about $0.60 that IBKR paid us on idle cash, not interest owed. The margin charge had not posted yet.

Margin is not the same as CFD leverage

It is worth drawing a clear line here, because the word "leverage" gets used loosely. A margin loan means you borrow cash to buy the real asset. You own the shares, you receive the dividends, and you pay interest on the loan. Some other platforms instead offer leverage through contracts for difference, or CFDs. With a CFD you do not own the underlying asset at all. You hold a derivative contract that tracks the price, you pay a daily financing fee for as long as the position is open, and the product is generally designed for short term speculation rather than long term holding.

For a buy and hold investor, genuine margin is almost always the better structure: you own the asset, the cost is a transparent annual interest rate rather than a daily financing charge, and there is no built in incentive to close the position quickly. CFDs carry their own elevated risks and are a different product entirely. If you are weighing the two approaches, it helps to understand both, and the distinction matters more than most beginners realise.

A worked example in dollars

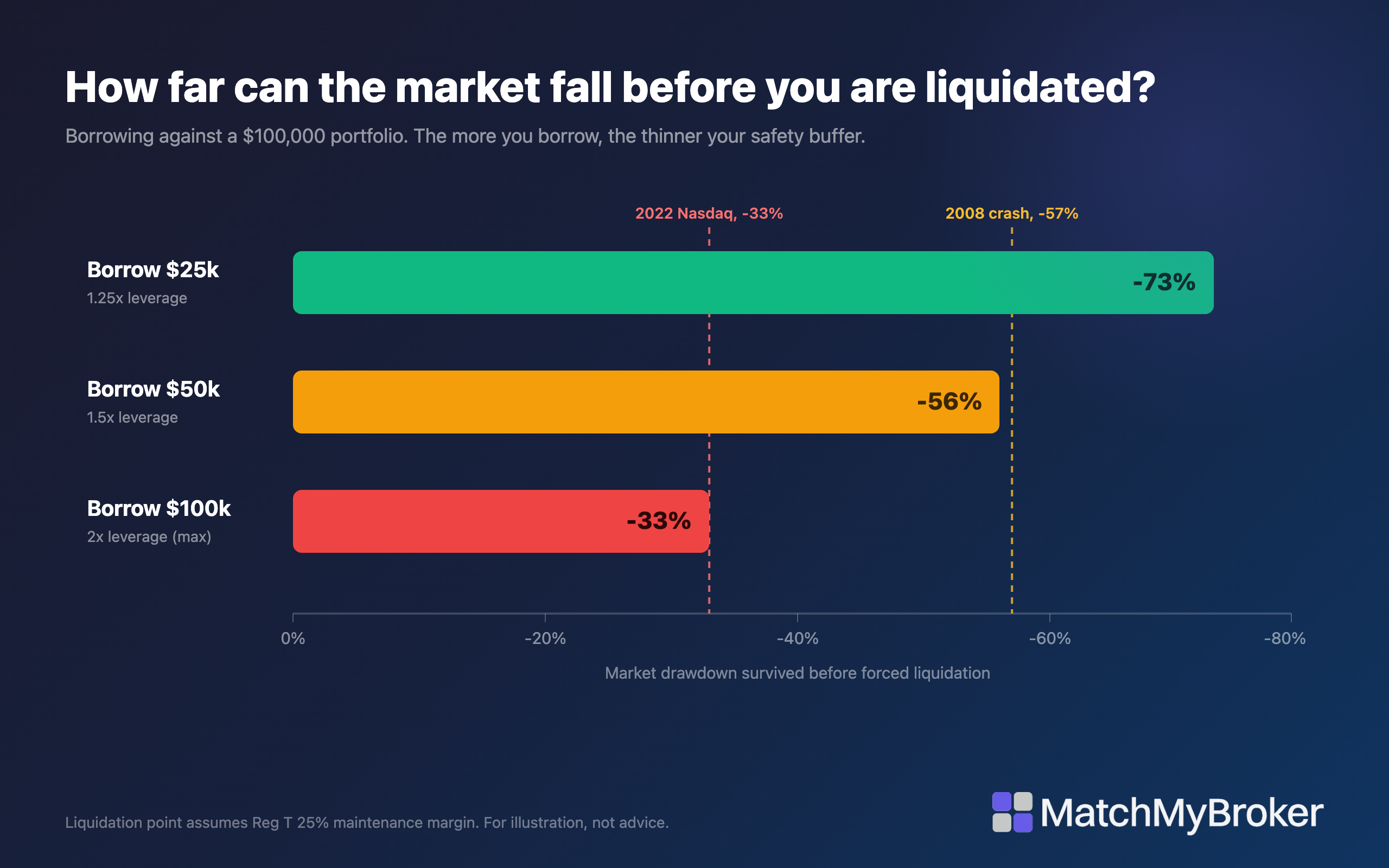

Numbers make this concrete. Imagine an investor with a $100,000 portfolio invested in a broad index ETF. They decide to borrow on margin to increase their exposure. The chart below shows three borrowing levels and, crucially, how far the market would have to fall before Interactive Brokers force closes the position.

The safety buffer shrinks fast as you borrow more. At the maximum loan, a 2022-style drop is enough to liquidate you. A conservative $25,000 loan would survive even a 2008-scale crash.

The pattern is clear. The more you borrow, the smaller the market drop needed to wipe you out. Borrow a conservative $25,000 and the market would need to fall 73 percent before liquidation, which has essentially never happened to a broad index over any short period. Borrow the maximum $100,000 and a 33 percent fall, roughly what the Nasdaq did in 2022, would force closure right at the bottom. That is the difference between leverage you can live with and leverage that ends your investment at the worst possible moment.

Now look at the return side. Borrowing $50,000 on that $100,000 portfolio and holding for a year produces the following, after deducting the interest.

Margin is symmetrical. It amplifies gains and losses by roughly the same factor, and it adds the interest cost as a small permanent drag whatever happens. In a flat year you are down 2.6 percent purely because of the borrowing cost. In a strong year the leverage clearly pays. This is why margin rewards a genuinely long time horizon: across many years a rising market is more likely, but in any single year you must be able to stomach the amplified downside.

When liquidation happens, and why it is different here

This is the single most important section. Interactive Brokers does not make margin calls. Most legacy brokers will phone you, email you, and give you a day or more to deposit funds before they touch your positions. Interactive Brokers does not. Its system monitors your account in real time and, the moment your equity falls below the maintenance requirement, it begins selling your positions automatically to bring the account back into line. It may send a deficiency notice on a best efforts basis, but it is under no obligation to reach you first, and in a fast moving market it often will not.

Two further points that surprise people. You do not get to choose what is sold. Interactive Brokers decides which positions to liquidate to protect its own interests. And the maintenance requirement is not fixed. The broker can raise its house margin requirements at any time, without notice, and it does exactly this during turbulent markets. Ahead of the 2020 US election it raised some requirements by as much as 35 percent, and during the March 2020 crash it lifted requirements on various holdings overnight. An account that looked safe on Friday could be in a forced liquidation zone on Monday.

The defence is straightforward: do not run close to the limit. Keep your borrowing well below the maximum, keep a cash or funding buffer you can deploy quickly, and set price alerts above your liquidation level so you have warning. The investors who get hurt are almost always the ones who treated the maximum buying power as a target rather than a ceiling.

This is also where it helps to know the two numbers Interactive Brokers shows for exactly this purpose. Maintenance Margin is the minimum equity your positions require, and Excess Liquidity is your buffer above that line. As long as Excess Liquidity stays comfortably positive, you are safe. As it approaches zero, you are approaching forced liquidation. Watching that single figure is the simplest way to monitor your real time safety, far more useful than the headline buying power number.

Our account carrying a small loan: Maintenance Margin of about $22,500 against Excess Liquidity of about $66,600. That gap is the cushion before any forced selling begins.

The quiet advantage: borrowing against cash that earns more

Here is an angle that rarely gets discussed. If you hold cash in a high yield savings account earning, say, 4 to 6 percent, and you borrow on margin at around 5 percent, the true cost of your leverage is close to zero, and in some cases negative. Rather than selling investments or draining your savings to buy more, you keep the cash earning its yield and borrow against your portfolio instead. The interest you pay on the loan is largely offset, or fully offset, by the interest your cash continues to earn.

This is the genuinely useful insight for anyone sitting on a meaningful cash balance for other goals, such as a property purchase, an emergency fund, or simply a deliberate cash allocation. Margin lets you stay invested without locking up that cash. The catch is that both rates move. If your savings rate drops well below your margin rate, the advantage disappears and the maths flips, so it is worth checking the spread every few months rather than setting and forgetting.

The honest risks

Margin works beautifully in a sustained bull market and punishes you in a falling or choppy one. The interest is a constant cost whether the market rises or not. The amplification cuts both ways, so a portfolio you were comfortable holding unleveraged can become genuinely stressful when every move is magnified. And the automatic liquidation means a sharp, temporary crash can permanently realise a loss that would have recovered if you had simply held.

It is also worth saying that leveraged products such as triple leveraged ETFs are a different and generally worse way to get daily leverage for long term holders, because they reset daily and decay in volatile markets. A plain margin loan against a broad portfolio avoids that decay entirely: you choose your own leverage ratio, you pay a known interest rate, and there is no daily reset eating your returns. For most long term investors who want measured leverage, a modest margin loan is cleaner than a leveraged fund.

Mistakes to avoid

- Treating buying power as spendable cash. It is the maximum the platform allows, not money you own. Anchor to your own equity instead.

- Borrowing without realising it. Buying a dollar denominated stock while holding only euros can quietly create a negative dollar balance that accrues interest, because the broker does not auto convert. Convert your currency first.

- Running near the maximum. The closer you sit to the maintenance limit, the smaller the drop that liquidates you, and the more vulnerable you are to a sudden house requirement hike.

- Expecting a warning. There is no courtesy call. Set your own price alerts and keep funds ready to transfer.

- Using margin on volatile single stocks. Concentrated or low priced shares can carry far higher margin requirements and far larger swings. Broad, diversified holdings are far safer collateral.

How to turn margin on at Interactive Brokers

Enabling margin is a simple account setting, not a separate application each time. You upgrade once, complete a short knowledge questionnaire, and the borrowing function is then available whenever you want it.

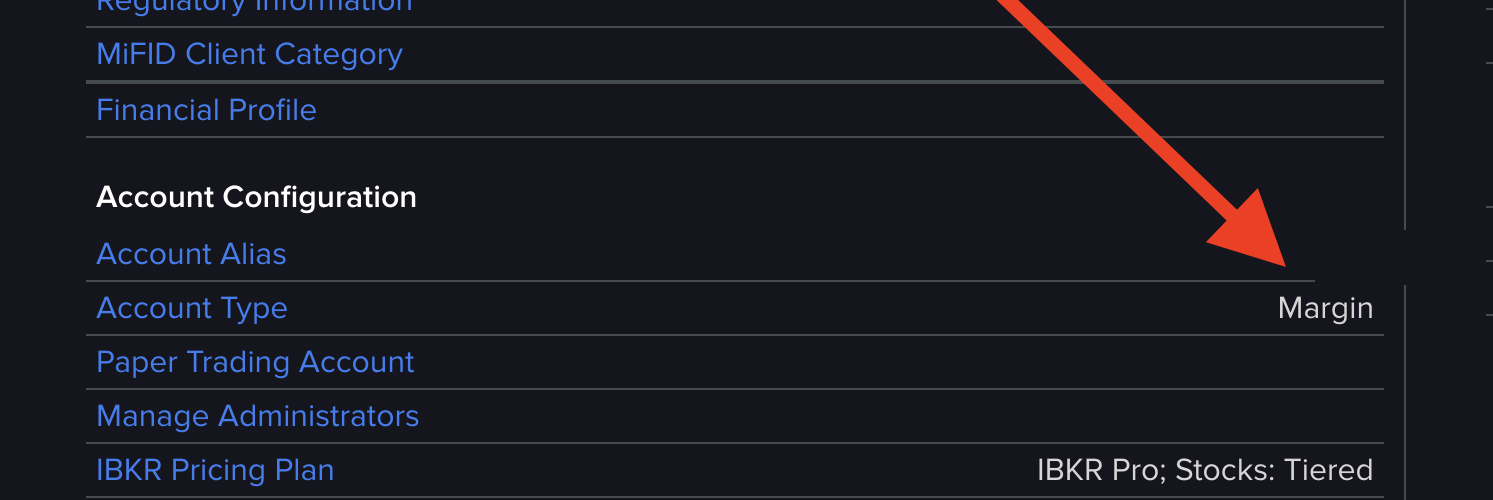

Once approved, the change is visible in your account settings. Under Account Configuration, the Account Type simply reads Margin, alongside the IBKR Pro pricing plan that determines the rate you pay.

After approval, our own Account Configuration shows Account Type set to Margin, on the IBKR Pro tiered plan.

The knowledge questionnaire is genuinely worth reading rather than clicking through, because the questions cover exactly the risks that catch people out, such as the fact that your potential loss can exceed your deposit and that positions may be force closed without notice.

If you decide margin is not for you later, the process reverses just as easily. Repay any loan by selling or depositing, then switch the account type back to Cash from the same settings page. There is no fee in either direction.

What we are doing ourselves

Since people always ask what we actually do rather than what we recommend, here it is, with the obvious caveat that this is not investment advice and you should reach your own conclusions. We recently switched our own Interactive Brokers account from a cash account to a margin account, and we have started using a modest amount of margin to add to our Nasdaq 100 position. We hold the European UCITS version, ticker XNAS, which tracks the same index as the better known US listed QQQ.

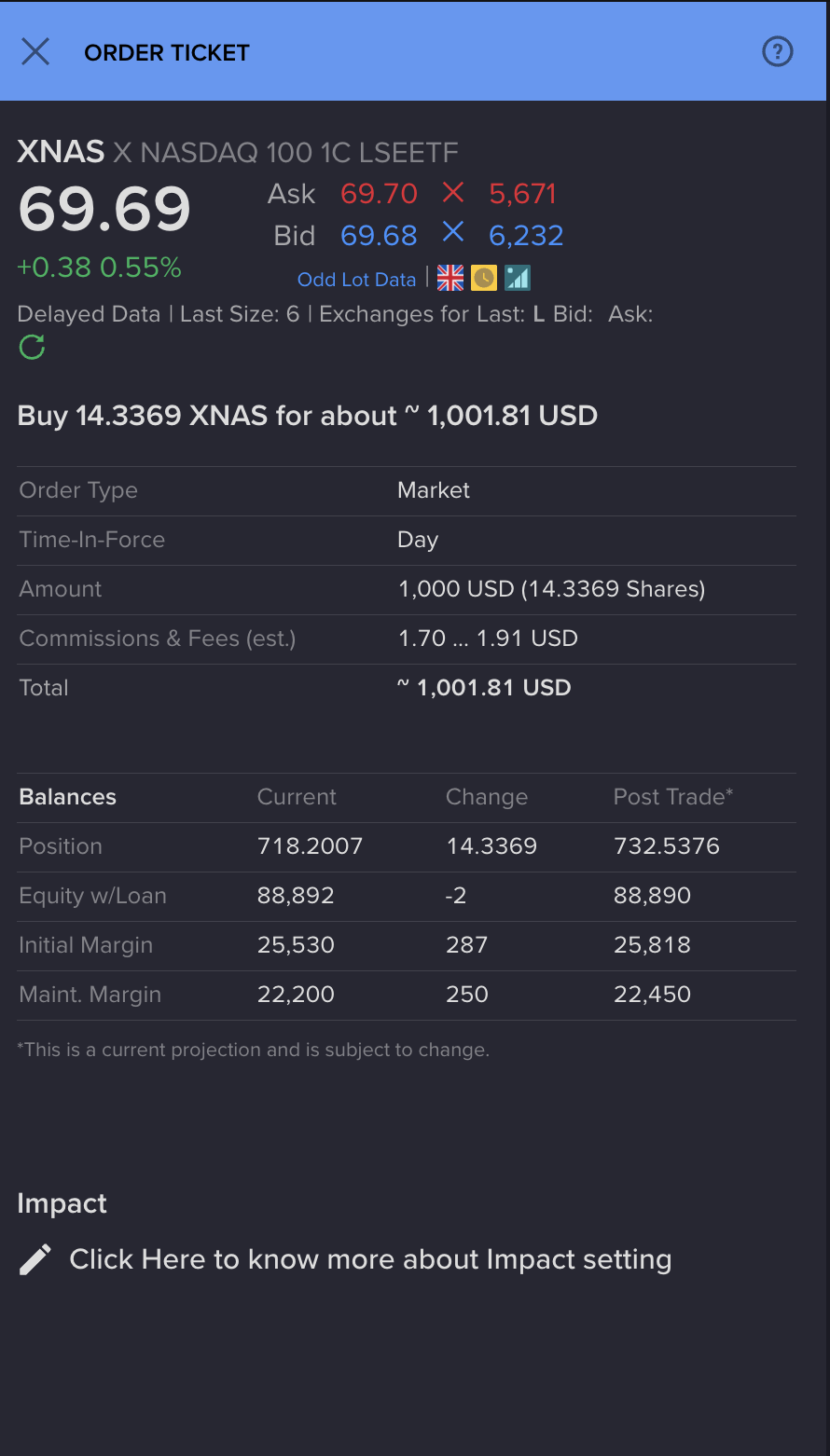

We started deliberately small. Our very first trade was a token position of around $1,000, placed purely to watch the mechanics work before committing anything meaningful. It was strangely useful to see it happen for real: the cash balance flipping negative into a small loan of about $900, the share count ticking up, the buying power adjusting, and the knowledge that a few cents of interest were now quietly accruing each day. For the price of a coffee or two a month, you get to learn exactly how the machine behaves with almost no risk. Only once that felt routine did we consider adding more.

Our actual first margin order: about $1,000 of XNAS. Notice the Initial Margin and Maintenance Margin lines updating, that is the requirement the trade consumes against your equity.

The reasoning is simple. We are confident in US technology over a long horizon, the borrowing cost is genuinely low, and we deliberately keep the loan well below the maximum so there is a wide margin of safety. Even a 2022 style fall of around a third would leave us a long way from any forced liquidation. We are not pretending leverage is risk free. It is a risk we are comfortable taking because the amount is small, the time horizon is long, and we can hold through a deep drawdown without being forced to sell.

We are also honest that this is not a fit for most people. It only works if you have a genuinely long time horizon, you can stomach an amplified drawdown without panic selling, and you keep the leverage conservative. If any one of those is missing, a plain cash account is the better and calmer choice, and there is no shame in that. But if you do share that long term conviction, in tech or in the broad market, and you size it sensibly rather than chasing the maximum buying power, a small slice of cheap margin can give your returns a real lift over the years. As always, it is your money and your call, so do your own research before acting on any of this.

Frequently asked questions

Will Interactive Brokers liquidate me if I have a margin account but do not use margin?

No. Holding a margin account does not mean you are borrowing. Liquidation risk only exists once your cash balance is negative, meaning you have actually borrowed. If you only ever buy with your available cash, the account behaves like a cash account and there is nothing to liquidate.

How is the margin interest calculated and when is it charged?

Interest accrues daily on the amount you have borrowed, at the tiered rate for your loan size and currency. It is posted to your account once a month, on the third business day of the following month. If you hold cash, the interest comes out of that cash. If you are fully invested, it is added to your loan balance.

Why is my buying power higher than what I deposited?

Buying power shows the maximum value of securities you could buy using margin, not money you hold. Interactive Brokers applies low margin requirements to diversified holdings and displays an intraday figure that can be several times your equity. Treat it as a ceiling to stay well below, not a target.

Will Interactive Brokers warn me before liquidating, and how fast does it act?

It does not make margin calls in the traditional sense. The system liquidates in real time when your equity falls below the maintenance requirement, and it may not reach you first. In fast markets the action can happen within minutes. Set your own price alerts above your liquidation level and keep funds ready to transfer.

What is the difference between Reg T and Portfolio Margin?

Reg T is the standard margin account, with 50 percent initial and 25 percent maintenance requirements. Portfolio Margin uses a risk based model that can allow higher leverage on diversified portfolios, but it requires a minimum account value of $110,000 and you become restricted if your equity falls below $100,000. Most investors start with Reg T.

How much margin is safe, and how far can the market fall before I am liquidated?

It depends entirely on how much you borrow. Borrowing a quarter of your equity might let the market fall around 70 percent before liquidation, while borrowing the maximum can mean a 33 percent fall is enough. A conservative approach is to borrow no more than 25 to 50 percent of your equity, which keeps the liquidation threshold far beyond any normal market drawdown.

What happens if my cash balance goes negative?

A negative cash balance is simply your margin loan. It can happen deliberately, by buying more than your cash covers, or accidentally, by buying an asset in a currency you do not hold, since Interactive Brokers does not auto convert. Either way you pay the margin interest rate on the negative balance until you repay it by selling or depositing.

Trading involves significant risk and may not be suitable for all investors. The value of investments can go down as well as up, and you may lose some or all of your initial investment. Past performance is not indicative of future results.

Kai is an investor who helps people choose the right broker and invest with confidence. He founded MatchMyBroker, a broker-comparison site for a global audience, and EU Investing Hub, his European-focused investing site. He also runs the Smart Money with Kai YouTube channel, where he breaks down investing, brokers and personal finance.